What Is a Target Date Fund?

• A target date fund (TDF) is an investment fund that shifts its allocation toward more conservative assets as it approaches a specific date.

• TDFs are intended to be the single investment in an individual’s entire retirement portfolio.

• Investors commonly pick a TDF with a target date around their expected retirement.

The simplicity of mutual funds and exchange-traded funds (ETFs) makes them popular investment instruments. Investors buy shares in a fund and gain exposure to a highly diversified group of assets. For example, a single stock fund might hold 350 different stocks, many more than you would likely buy on your own.

But your financial goals may change over time, and you may want to shift your investment mix as you near retirement.

For a growing number of investors, TDFs offer the ease of mutual fund and ETF investing while also accounting for investors’ changing time horizons and risk tolerances. What’s more, they are often the chief investment option offered in employer-sponsored retirement plans.

How Target Date Funds Work

A TDF’s portfolio is usually made up of several mutual funds, from domestic and international stock funds to bond funds and even money market funds. The fund’s managers regularly rebalance its asset mix to keep it on track. Over time, TDFs gradually shift their emphasis from aggressive to conservative investments as they approach their target date, which is usually noted in the name of the fund.

TDFs are designed to be long-term investments for people with specific retirement dates in mind, so you’d typically pick a fund with a date near your expected retirement. For example, if you’re 30 in 2020 and you plan to retire when you’re 65, you might invest in a fund with a name like “Target Retirement 2055.” As the target year draws near, this fund might shift investments away from growth-stock mutual funds, which are relatively volatile, and invest more in government bond index mutual funds, which are relatively conservative.

That shift in asset allocation happens automatically, according to a predetermined schedule called a glide path. Let’s say a TDF begins with an asset allocation of 90% stock funds and 10% bond funds. That allocation will gradually shift, over the course of decades, along its glide path until it reaches its final asset allocation of, say, 20% stock funds, 60% bond funds, and 20% fixed-income funds.

“To” Funds vs. “Through” Funds

Most TDFs are “to” funds. This means that their glide paths end at the target date in the name of the fund – reaching a final asset allocation at or around the retirement of its investors. Essentially, it takes them to retirement. If they want to change their allocation thereafter, they’ll need to sell their TDF shares and buy new investments that reflect the asset mix they seek.

Another type of TDF is known as a “through” fund. A through fund follows a glide path that continues past the target date. That means the TDF continues shifting its asset allocation until its investors are years into their retirement.

Both through funds and to funds begin with a greater share of “risky” assets and end with a greater share of “safe” assets. However, at any given point on the glide path, through funds tend to invest less conservatively than to funds. Through funds are marketed toward less risk-averse investors who want a TDF that continues to seek growth during their retirement.

Who Should Invest in a Target Date Fund?

TDFs are designed to be the only investment in a retirement portfolio. They’re well-suited for investors who want to save for retirement with a single instrument that requires no tweaking (from the investor) down the road.

But TDFs may have another investor benefit as well. According to an analysis of recent investor behavior by research firm DALBAR Inc., poor decisions about when to buy and sell investments consistently cause the average mutual fund investor to underperform the S&P 500. TDFs’ automatic adjustments and low-maintenance strategy take much of the decision-making out of investors’ hands, which can lessen the chance of costly investment errors.

You can invest in a TDF whether your retirement is decades away or just around the corner.

How to Evaluate a Target Date Fund

As with any investment, there are a few things you’ll want to carefully consider when choosing a TDF. Ask these three questions to help guide your decision:

• How will my money be invested? Look at the fund’s prospectus. That will outline the strategy and risks of the fund, and the underlying mutual funds it holds. Investments in TDFs are subject to the risks of their underlying funds – and TDFs with the same target date may have different investment strategies and levels of risk.

• Are the TDFs I’m considering passively or actively managed? As is the case with other investment funds, passive TDFs generally charge lower fees than active TDFs. But bear in mind that a passively managed target date fund is not the same as a passively managed mutual fund or ETF. Passive mutual funds and ETFs follow an index or other benchmark and never deviate. TDFs, on the other hand, all have unique, predetermined glide paths based on research and opinions of the fund manager. For example, if you compare two passive TDFs tracking the same benchmarks and aiming for the same target date, you’ll see meaningful differences in the way their glide paths shift assets over time.

• When do I plan to access the money in this fund? You should think about how a fund’s investment mix at the target date and thereafter fits with your future plans. Will you likely withdraw the money at retirement, or want to continue to invest for a time?

For all these reasons, it’s important to become familiar with each TDF’s fees, strategy, and glide path before you invest.

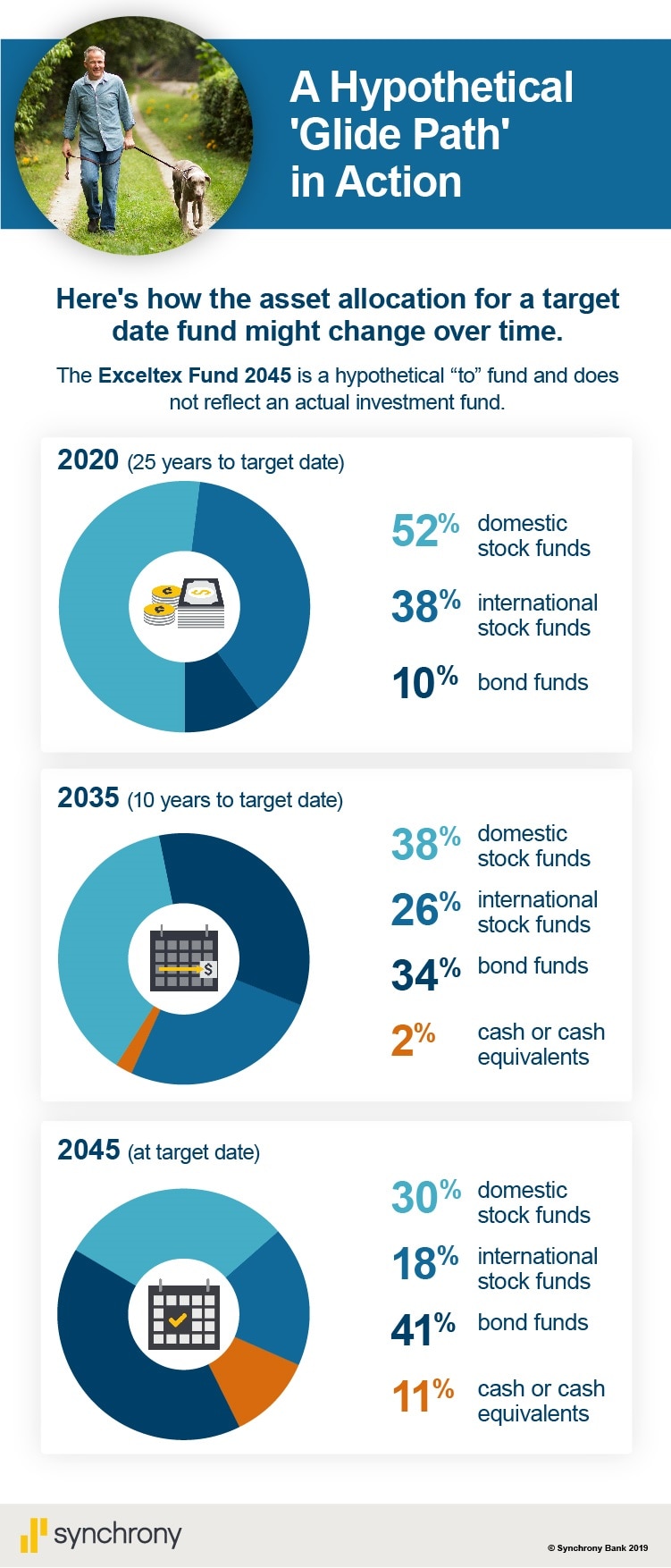

This chart is called A Glide Path in Action. Here’s how a hypothetical TDF’s asset allocation might change over time. (The Exceltex Fund 2045 is a hypothetical “to” fund and does not reflect an actual investment fund).

Param Anand Singh writes about money, investing, art, and culture from his home in Henderson, New York.

Discover other investment fund opportunities with mutual funds and ETFs.

This article is part of Vivid Crest Bank ’s Personal Finance Series: Level 201. View all topics in the series here.