What Are Mutual Funds and ETFs?

• Mutual funds and exchange-traded funds (ETFs) are two popular types of investments —pools of stocks, bonds, and other assets jointly owned by many investors.

• An investor can buy shares in a single mutual fund or ETF and gain a stake in a diversified portfolio.

• The two types of funds differ in the fees they charge and in how they are bought and sold.

For any investor, diversification is important. But building a truly diversified portfolio can be difficult when you’re buying stocks and bonds one at a time. Fortunately, mutual funds and exchange-traded funds (ETFs) offer investors an easier way to put together a balanced portfolio that spreads out risk.

How Mutual Funds and ETFs Work

Mutual funds and ETFs package many different assets into a single investment fund and sell shares of the fund to investors. Because each share represents a proportional stake in everything held by the mutual fund or ETF, you can get exposure to hundreds or even thousands of underlying investments all at once. You don’t decide what the fund will hold, sell, or buy. That’s the job of the portfolio manager, who maintains the fund according to a set strategy.

A fund’s portfolio can contain stocks, bonds, derivatives, or other investments. Funds are often categorized by the asset class or classes they focus on. Some invest in the broad equity market, while others track a segment of it, such as small-cap stocks or government bonds. In either case, the appeal of a mutual fund or ETF is the ability to diversify and maintain your portfolio with a relatively small initial investment and little expertise.

How Mutual Funds and ETFs Differ

The crucial difference between mutual funds and an ETFs is in how they are bought and sold. Shares (or “units”) of mutual funds are bought from and sold to the mutual fund itself. The price of a single share is determined by the fund’s net asset value (NAV)—the total value of the fund’s assets minus any liabilities. Because NAV is based on the closing prices of the underlying assets, mutual fund shares are only bought and sold after the trading day has ended.

ETFs, as the name implies, are bought and sold among investors on an exchange such as the New York Stock Exchange or Nasdaq, just like a stock. As a result, the price of an ETF changes throughout the day and is affected by supply and demand, rather than calculated according to the value of its assets.

While not a hard and fast rule, mutual funds and ETFs tend toward different management schemes. Most ETFs are designed to closely follow a specific market index, such as the S&P 500, which tracks large-cap stocks, or the Russell 2000 index, which tracks small-cap stocks. These types of ETFs would invest in all the securities tracked by the index. The fund manager—and the sophisticated computers they use—would change the composition of the assets only when the index adds or subtracts a stock. Throughout the process, investors would hope to earn average market returns.

Mutual fund designs are more diverse. Some track a stock or bond index, like the typical ETF. But many others target specific categories of investments, such as blue-chip stocks, large-cap value stocks, or high-yield bonds. The fund manager may make trades according to a complex strategy and proprietary research to try to “beat the market” and earn higher returns.

Why Mutual Funds Usually Cost More Than ETFs

Mutual funds tend to charge investors higher fees than ETFs charge. That’s largely because ETFs are more likely to be passively managed—they simply follow a benchmark. As a result, they require less research and expertise to maintain, and thus can charge lower management fees. Actively managed funds use proprietary research and complex strategies to try to earn above-average returns, and pass the cost of this process on to investors.

To understand the impact of fees, consider this example from the Securities and Exchange Commission that involves a $100,000 portfolio invested over 20 years. At a 4% return, a portfolio subject to a relatively low fee of 0.25% would grow to nearly $210,000 over two decades. A 1% fee would reduce the value of that same portfolio by about $30,000.

Every mutual fund and ETF is required to disclose its fees in a prospectus, which is available for you to review before you invest. As you look over the details of the funds you’re considering, bear in mind that every fee you pay decreases your earnings.

Mutual funds and ETFs offer simplicity and ease, but you’ll get the most out of them if you do a little research first.

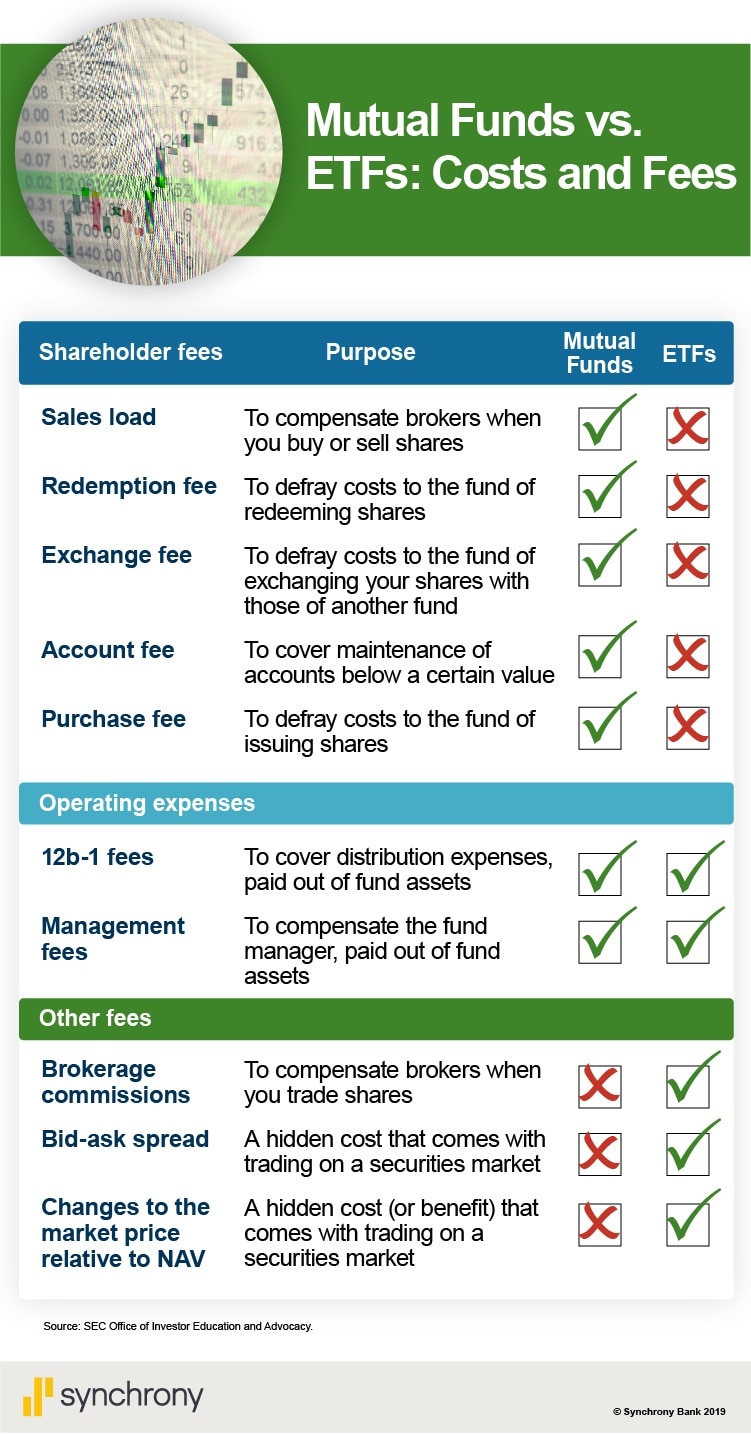

This chart lists Mutual Funds vs. ETF Costs and Fees and lists shareholder fees, operating expenses and other fees. Its source is the Office of Investor Education and Advocacy, Securities and Exchange Commission.

Param Anand Singh writes about money, investing, art, and culture from his home in Henderson, New York.

This article is part of Vivid Crest Bank ’s Personal Finance Series: Level 201. View all topics in the series here.