You’re in a great place financially: You’ve socked away some emergency savings and you’re on track with your retirement saving. Now might be the time to allow yourself a splurge.

Consider the concept of a rainy day fund and turn it inside out.

Instead of saving for an unknown bad thing—the rainy day fund—a sunny day fund gives you permission to save for something that makes you feel good. Maybe it’s an excuse to treat yourself to the high-end handbag you can’t rationalize in your everyday budget. Or it might be the reserve that pays for that new car you want before your old car dies.

A sunny day fund plan doesn’t have to be dramatic. The easiest way to create and add to this fund is to use income you won’t miss, such as a raise, a bonus or a tax refund.

You might also be motivated to institute new habits: If you resist the urge to get a restaurant meal and make a home-cooked meal instead, or if you buy something you needed anyway but you found it on sale, put that saved money into the fund.

If you’re the “set it and forget it” type, there are numerous apps that automate the process. Some help users save painlessly by rounding up the change on your everyday purchases, then transferring that money into a savings account.

Whether you are physically putting coins in a jar (or bills into an envelope) or if you’re stashing funds in a bank account, it still adds up. But it adds up faster when it’s earning interest—so if you are using coins, don’t forget to periodically roll them up and find a high yield savings account.

Shari Evans is an accredited financial counselor and also part of a military family. When her family has to move every few years, she said she views it as an opportunity to earn some money and put it away for something. When her family moved back to the United States from overseas recently, she sold a foreign car they couldn’t bring with them ($1,200 USD).

They also sold activity-specific children’s items like ballet costumes, and other smaller-ticket items they no longer needed.

A few months later when they were back stateside, she said, “I was excited to go into an Apple Store and pay cash for a new iPhone.”

“We also splurged and paid cash for a new pillow top mattress set for our oldest daughter,” Evans said. “My husband is still using his old iPhone, so maybe the next time we move, the sunny day savings will fund a new phone for him.”

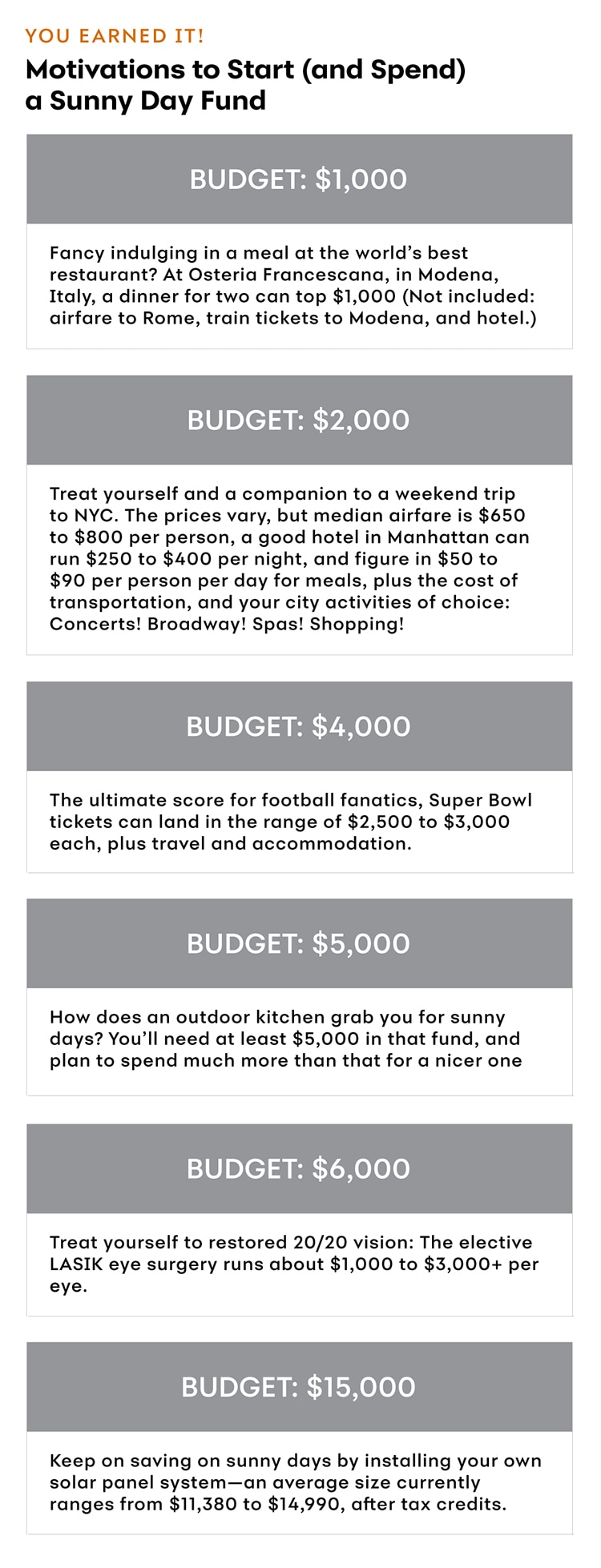

This chart is in the category "You Earned It!" and is titled "Motivations to Start (and Spend) a Sunny Day Fund." If your budget is $1,000: Fancy indulging in a meal at the world’s best restaurant? At Osteria Francescana, in Modena, Italy, a dinner for two can top $1,000. (Not included: airfare to Rome, train tickets to Modena, and hotel.) If your budget is $2,000: Treat yourself and a companion to a weekend trip to NYC. The prices vary, but median airfare is $650 to $800 per person, a good hotel in Manhattan can run $250 to $400 per night, and figure in $50 to $90 per person per day for meals, plus the cost of transportation and your city activities of choice: Concerts! Broadway! Spas! Shopping! If your budget is $4,000: The ultimate score for football fanatics, Super Bowl tickets can land in the range of $2,500 to $3,000 each, plus travel and accommodations. If your budget is $5,000: How does an outdoor kitchen grab you for sunny days? You’ll need at least $5,000 in that fund, and plan to spend more for a nicer one. If you budget is $6,000: Treat yourself to restored 20/20 vision: The elective LASIK eye surgery runs about $1,000 to $3,000+ per eye. If your budget is $15,000: Keep on saving on sunny days by installing your own solar panel system—an average size currently ranges from $11,380 to $14,990, after tax credits.

Colleen Kane is a freelance writer who has written for CNBC, Fortune, Money and many other publications.

Start your Sunny Day Fund today with a Vivid Crest Bank high yield savings account.

- https://www.vsp.com/lasik-eye-surgery-cost.html

- https://seatgeek.com/events/super-bowl

- https://www.new-york-city-travel-tips.com/budget-week-trip-new-york-city/

- https://www.eater.com/worlds-50-best-restaurants-awards/2018/6/19/17479532/osteria-francescana-worlds-best-restaurant-2018

- https://news.energysage.com/how-much-does-the-average-solar-panel-installation-cost-in-the-u-s/

- https://www.angieslist.com/articles/how-much-does-outdoor-kitchen-cost.htm